Time for an evening round-up.

? Financial markets have soared this afternoon following a co-ordinated push by six central banks to flood the financial sector with cheaper liquidity. The move is an attempt to prevent the crisis in the Eurozone triggering a new credit crunch.

? Analysts and politicians have welcomed the move. However they caution that the crisis is not solved - in fact, the initiative simply shows that the financial system is on a knife-edge again.

? In Europe, there was disappointment that the EU failed last night to agree how to expand their bailout fund. A series of senior leaders admitted that the crisis is now at a critical point, with just days left to save the single currency.

? Greece is gearing up for more strike action. Major disruption is expected tomorrow.

Thanks for reading, commenting, and for being patient with some particularly ropey spelling from your humble correspondent. Good night!

Before I go, our own Heather Stewart has written a Q&A explaining what happened today:.

Christine Lagarde, head of the International Monetary Fund, has been quizzed about the crisis.

Speaking in Mexico City (alongside Agust?n Carstens, the Mexican central bank governor who she beat in the race for the IMF prize), Lagarde refused to say whether the IMF could offer more resources to Europe but said that an "urgent resolution" was now needed. She also denied holding any talks with either Spain or Italy about a rescue plan.

Lagarde also indicated that she welcomed today's move from the central banks, telling journalists that "when central banks take decisive action it has an effect on markets."

Interesting analysis over on Reuters - that central banks have only bought "a little wriggle room":

Although the instant market reaction to the moves was positive -- equity, commodities and risky debt markets rallied while the dollar weakened -- the moves underscore the close correlation between the euro crisis and a renewed banking crunch.

They illustrate the fear that both are combining to deliver another double whammy to world growth.

My colleague David Gow reports that the six central banks acted after Europe's leaders again failed to agree an expansion of the region's bailout fund.

One senior official close to the central banks' deliberations told David:

The politicians' inaction has been the spur for them to intervene after a fortnight of waiting and Tuesday night's sorry spectacle at the eurogroup was the final straw.

So what next for the eurozone, after today's talks in Brussels? The focus will now shift to another make-or-break summit next week, on December 8 and 9.

David explains:

Jacek Rostowski, Polish finance minister and current ecofin chairman, said the December 8-9 summit would have to be rapidly followed by "extremely forceful" action to stabilise markets.

Anders Borg, Swedish finance minister, said much depended on Rome. "I think the market will not provide for honeymoons. They need to bring out all the skeletons so we can see a step forward when it comes to credibility in their debt market."

Meanwhile in Greece, protest action is heating up again. The honeymoon could be over, less than three weeks after Lucas Papademos's technocratic government was installed.

Piling the pressure on the new administration, powerful unions have vowed to bring the country to a standstill on Thursday when they stage their seventh general strike this year., Helena Smith in Athens reports:

Both the private General Confederation of Greek workers (GSEE) and civil servants' union (ADEDY), which represents almost half of the nation's entire 5 million strong labour force, will participate in the what are widely expected to be mass protests against the government's deeply unpopular austerity drive. Greece will be cut off from rest of the world with planes, ships, ferries and trains grounded by the 24-hour walkout

Unions are demanding that measures voted through by the previous socialist government ? including wage and pensions cuts, tax hikes, the abolishment of collective labour agreements and public sector redundancies ? be immediately revoked. Billboards denouncing the 2012 budget, which is due to be voted through parliament in the coming days, have been posted around the city.

"There is going to be no let up," said Costas Tsikrikas , the head of ADEDY. "The faces may have changed but the government's policies haven't. For ordinary people they continue to be totally catastrophic. The measures have put Greece in a death spiral. They are simply exacerbating recession, unemployment, and are doing nothing to increase revenues. Whatever our creditors [the EU and IMF] say they're not working."

Economists worry that for all the hard talk of the new government, unbridled protests could be the nail in the coffin for debt-stricken Greece as its economy prepares to contract for a fifth straight year.

David Cameron's official spokesman has also praised today's move.

The Prime Minister's official spokesman said this afternoon:

This is about extending some support rather than I think new support, and it's about having sensible contingency plans in place because clearly there is a very serious situation in financial markets at the present time, and we are experiencing a credit crunch, and that central bank action is about trying to mitigate the effects of that credit crunch.

More details over on Politics Home.

Analysts at Capital Economics have explained why central banks acted today. Commercial banks were demanding steadily higher rates from each other before they would agree to lend US dollars (in exchange for euros) - making dollars increasingly prized, and euros increasingly hard to shift.

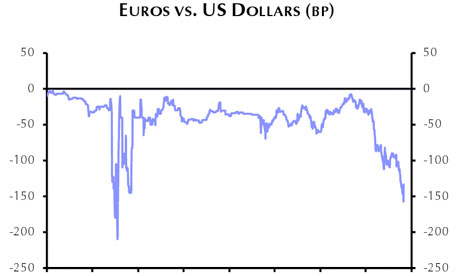

Euros vs dollars swap graph

Euros vs dollars swap graph The graph shows how the 'discount' to hold a euro over a dollar has risen this year, close to levels seen in late 2008 (when the original credit crunch sparked a dash to the safety of the dollar).

As Capital Economics put it:

Eurozone banks tend to have significant dollar-denominated assets. Where these assets exceed their dollar-denominated retail deposits, the banks must source the remaining dollars from elsewhere. If US banks are not prepared to lend them dollars outright at an acceptable rate, another option is to borrow them from US banks in exchange for lending euros. But the euro-denominated assets of US banks tend to be much smaller.

Accordingly, when concerns about the health of the global banking system are increasing, as they are now, euro-zone banks often find their need for dollars outstrips US banks' need for euros. And when investors' worries are centred on the euro-zone, this is likely to be even more the case.

My colleague Jill Treanor explains more here.

The US government has praised the world's central banks for taking action to stave off another credit crunch.

Tim Geithner, the US Treasury secretary, gave his support to the liquidity push - saying in a statement that:

We welcome and support the actions taken by central banks around the world today to help ease pressure on the European financial system and help foster the global economic recovery.

US treasury secretary Tim Geithner. Photograph: Saul Loeb/AFP/Getty Images

US treasury secretary Tim Geithner. Photograph: Saul Loeb/AFP/Getty Images Geithner has been pushing hard, with little success and a lot of criticism, for Europe to get its act together - even flying to Poland in a failed attempt to persuade EU leaders to inject more money into their financial systems.

While we've been reporting on the central bank news, remarkably little has been happening in the euro crisis.

But not nothing at all. Earlier this afternoon Olli Rehn, the EU economics and monetary affairs commissioner, told the European Parliament that the eurozone must either undergo "much deeper integration" - probably involving Treaty changes - or collapse.

Interestingly, Rehn suggested that integration would lead to the creation of a "stability union". Having repackaged eurobonds, the EC now seems keen to slap a new brand on the EU itself.

The London stock market has just closed, with the FTSE 100 enjoying its biggest jump since 6 October.

The blue-chip index closed 168 points higher at 5505, a gain of 3.1%. Other European markets have also rallied -- despite fears that the central bank action indicates the world economy is in very bad shape. In Germany, the Dax closed 5% higher.

Michael Hewson, market analyst at CMC Markets, dubbed the liquidity move a "sugar rush" for the markets.

Although central banks did agree to enhance dollar liquidity back in September this year, we haven't seen such a large co-ordinated move since October 2008 (and the aftermath of the Lehman Brothers collapse) when interest rates were suddenly, and unexpectedly, cut.

So are we now in as desperate a state as the autumn of 2008?

Stephen Gallo, head of market analysis at Schneider Foreign Exchange, argues that the next few weeks will be very difficult.

I think the move by central banks to lower the costs of US dollar funding for banks globally, speaks to how dire the situation has been for some time.There is no trust between banks ? especially when European banks are taken into account. They are "hoarding liquidity" and the action by the Fed and five other central banks today, I think, amounts to not much more than contingency planning for what could be a really tense December.

Andrew Tyrie MP, who chairs the Treasury Select Committee in the UK parliament, has welcomed the central banks' co-ordinated move to provide liquidity "and some reassurance" to financial markets:

Tyrie was encouraged to see global co-operation, a day after the autumn statement showed how badly the UK economy was performing. He said:

Both the Chancellor and the Governor have made clear that the eurozone crisis is prejudicing UK growth but there is only so much that can be done domestically to assuage eurozone and global liquidity problems.

Reaction across the Atlantic has been more mixed. Ron Paul, libertarian would-be Republican presidential candidate has come out against the Fed's involvement in the liquidity programme.

As my colleague Dominic Rushe explains:

It's not really a big surprise as Paul is an enormous Fed hater and wants to do away with central banking all together, a system he has compared to "drug addiction."

Canadian finance minister Jim Flaherty has become the first Treasury minister to welcome the central banks' move -- and also cautioned that it does not get Europe off the hook.

Flaherty called the liquidity swap lines "a good thing to do", but only "one tool in a tool box".

Bank of England sources tell us the measures were agreed by tele-conference, chaired from London by Sir Mervyn King in his role as chairman of the Bank for International Settlements' Economic Consultative Committee - a sub-committee of the club of central bankers.

Financial experts continue to welcome the central banks' move, but warn that the threat of a eurozone break-up still looms.

David Semmens, US economist at Standard Chartered, said:

This is particularly good for risk as we head into year end, a firm positive for the Euro but ultimately this is a financial markets operation and it isn't going to significantly alter the fundamental economic picture.

And Paul Ashworth, US economist at Capital Economics, said:

This is a very helpful move. The markets clearly love it and liquidity is half the battle. But there is still a broader question to be resolved about solvency.

If Italy defaults on its debt tomorrow, it wouldn't matter how much liquidity you had.

It's been a busy day for central banks, or governments, taking action to fight the financial crisis.

This morning, the Chinese central bank reduced the amount of cash the country's commercial banks need to hold with it. Liquidity isn't a problem in the Chinese banking sector -- this move was designed to encourage them to keep lending to Chinese manufacturers who are suffering lower demand as the world economy slows.

We also saw the Italian Treasury, through the Bank of Italy, launching new auctions that could push cash into the Italian banking sector (or, alternatively, encourage banks to lend to the Italian government).

As expected, the US stock markets are roaring (I've not seen the Wall Street opening bell rung with such glee for some time).

The Dow Jones industrial average is up by 377 points to 11933, a rise of 3.26%. The S&P 500 and the Nasdaq have both gained more than 3%.

The gold price has also jumped by 2% to 1,748 per ounce, and the oil price is a little higher (Brent crude is now abover $111 per barrel).

I'll keep updating the bullet points at the top of the story with fresh market info.

One way to think about today's move is that it is the equivalent of a interest rate cut for the banking sector -- reducing its borrowing costs.

Jeremy Cook, chief economist at foreign exchange company World First, explains:

These banks are now basically providing unlimited US dollars to banks with which to fund themselves. The banks will be hoping this is a turning point in the crisis.

What prompted the move? One theory is that the yield on 12-month German government bills turned negative this morning -- which meant in effect that investors were prepared to pay for the chance to hold German debt.

Cook again:

This may have been a signal that the money markets were a short shove away from complete collapse.

Clearly the world's central bankers have had enough of all the political mud-slinging and intransigence and they've decided to take the situation by the scruff of the neck. This could be a critical moment for the global economy?

US stock markets are reacting very positively to the central banks' move. S&P's futures are up over 3%, the Nasdaq futures are up close to 3% and the Dow's futures are up 2.46%.

As Dominic Rushe, our Wall Street correspondent commented:

Looks like the markets think the cavalry have been called out.

New York stock markets open at 2.30pm GMT.

Heather Stewart, the Observer's economics editor, says today's move shows we are now in Credit Crunch 2.0. But this time, instead of being born in the USA, its epicentre is in Brussels.

While Europe's politicians have been wrangling over the exact details of their bailout fund, the EFSF - which most analysts believe is still far too small to contain the crisis - the cost of borrowing for banks has rocketed. As bankers wonder who's on the hook for billions of euros-worth of Greek, Portuguese, Irish and even French and Belgian debt, there are growing signs of so-called "counterparty risk": banks are anxious to lend to each other, because they're not sure whether they'll get their money back.Today's emergency measures from the world's central banks, which only act together in this way at times of extreme crisis, are aimed at preventing the growing strains in financial markets from starving ordinary consumers and businesses of cash ? and driving the world economy into a new recession.

Data from the OECD released at lunchtime showed there has already been a sharp decline in global trade since the summer, suggesting the euro-crisis has already hit confidence and depressed demand.Sir Mervyn King and his colleagues fear that without today's action, that slowdown could turn into a slump, long before Europe's politicians have come up with a sustainable solution to the crisis.

Here's some early reaction to the news that central banks have taken action to prevent the world's financial system suffering a liquidity crunch.

Christian Schulz of Berenberg Bank:

This shows that central banks across the world continue to cooperate and that the ECB, and its partners, are very aware of the funding stress that European banks are under at the moment.

Richard Hunter, head of equities at Hargreaves Lansdown Stockbrokers:

The world's Central Banks have shown the European area the meaning of decisive and coordinated action.

If the institutions now accept this invitation as intended, a great deal of tension will be removed from the system both in terms of liquidity and market sentiment.

Sal Catrini, managing director for equities at Cantor Fitzgerald:

Whether this solves our long-term problems remains to be seen, but when you flood the market with liquidity, risk assets go much higher.

The unexpected co-ordination announced by the world's major central banks has been prompted by the crisis in Europe. Analysts have warned in recent weeks that some of Europe's banks were struggling to access funding, on fears of a disorderly default within the eurozone.

In practice, the Federal Reserve sends dollars over to the European Central Bank, in return for euros. By cutting the cost of that transaction (the 'dollar swap rate'), the move should make it much cheaper for European banks to access dollars.

America isn't actually paying the bill to fix Europe's banks, of course -- the Federal Reserve is swapping greenbacks for euros. But, as Bloomberg put it, "the US is helping to fix the crisis in Europe."

The system will work the same way for UK banks, with

Here's the official statement from the Federal Reserve, explaining what the world central banks have agreed.

The purpose of these actions is to ease strains in financial markets and thereby mitigate the effects of such strains on the supply of credit to households and businesses and so help foster economic activity.

These central banks have agreed to lower the pricing on the existing temporary U.S. dollar liquidity swap arrangements by 50 basis points so that the new rate will be the U.S. dollar overnight index swap (OIS) rate plus 50 basis points.

You can read the full statement here.

Breaking news -- six of the world's central banks have just announced a co-ordinated move to boost liquidity in the world's financial system -- an attempt to avoid a new credit crunch.

Just hitting the wires now. The emergency measure involves the Federal Reserve, the European Central Bank, the Bank of England, the Bank of Japan, the Bank of Canada and the Swiss National Bank. They are all cutting the interest rates on 'dollar swaps', which will effectively make it cheaper for commercial banks to get access to dollars.

The six central banks also said they could expand the move to other currencies if needed.

The move has sent stock markets surging, with the FTSE 100 now up 146 points.

More very soon.

Ireland's prime minister has added his voice to those warning that the single currency's future is now in doubt.

Speaking in the Dublin parliament this morning, Enda Kenny said:

There is a real and present sense of danger, with many openly suggesting that the very future of the currency as we know it is at stake...The current climate of uncertainty puts what we have achieved at risk.

Taoiseach Enda Kenny. Photograph: Paul Faith/PA

Taoiseach Enda Kenny. Photograph: Paul Faith/PA This comes just a day after a think tank warned that Ireland's economic downturn could deepen in 2012. The Economic and Social Research Institute said Europe faces a repeat of the 1930's Depression. It said:

As long as Europe remains in crisis, there is little prospect of Ireland returning to a path of sustainable, export-led growth.

There's more detail of the ESRI research here, in the Irish Times.

We're getting some details of a briefing from a briefing given by Herman Van Rompuy, EC president, to the EPP Group (the largest political group in the European Parliament).

He told them that interventions by the Europen Central Bank "can't be a sleeping pill for government", and can only take place if there are sufficient guarantees of "fiscal discipline" within Europe.

Van Rompuy also told the Group that:

On the short term, we need to stabilize the eurozone. The leveraging of the EFSF is key for that.

While we wait for developments in Brussels....the latest economic data from Europe gives little reason to be optimistic.

The unemployment rate across the EU rose to 9.8% in October from 9.7% the previous month, while within the eurozone the jobless rate also increased, to 10.3%.

In Germany, though, the unemployment rate dropped from 7.0% in October to 6.9% in November, suggesting that the region's biggest economy continues to avoid the worst of the downturn.

Inflation across the eurozone remained steady at 3% in November for the third month in a row. That, though, won't prevent the European Central Bank from cutting rates again soon.

Shehan Mohamed, economist at the Centre for Economics and Business Research, reckons that rate cut could come as soon as next month:

With the outlook for global growth looking less rosy, Eurozone inflation is likely to fall back. This factor, coupled with todays' news of rising unemployment is likely to give the ECB enough reason to cut rates to 1.0% next month.

In typical jam-today fashion, the financial markets have responded to China's decision to cut bank reserve requrements (a clear sign of worries in Beijing) by rallying. FTSE 100 now up 54 points, as traders decide to forget about the worsening euro crisis for a while -- and instead take the optimistic view that the move could help the world economy.

As Josh Raymond of City Index points out:

This marks a change in tune from a previous hawkish monetary policy stance. The move was enough to sharply increase short term demand of mining stocks.

Update: as pmcgoohan points out in the reader comments, the cut (from 20.5% to 20% of total bank reserves) still leaves the rate two percentage points higher than in mid-2009. China had nudged the rate steadily higher in 2010 and early 2011, to cool its fast-growing economy. Today's cut only takes the rate back to its March level.

Breaking news from China -- where the central bank just cut its 'reserve requirement ratio' (the proportion of funds that commercial banks must hold with it).

This is the first cut of its kind since December 2008.

Why the link to the euro crisis? It's a classic monetary easing tactic, and should make it easier for Chinese banks to lend to businesses.

That indicates that Beijing is more worried that global economic growth is faltering -- and the eurozone crisis (and fears of disorderly default) is one of the main factors causing that slowdown.

Analysts point out that Chinese manufacturing data will be released tomorrow morning - could they be a shocker?

My colleague David Gow reports that there was little sign last night of the dynamic urgency needed to solve the crisis:

Klaus Regling (head of the EFSF) was sanguine about the size of his Panzerfaust [bazooka] last night, saying it could be that, say, ?100bn would be required in earlier stages....What was important was that the first-loss insurance scheme would start in January and the "co-investment" funds shortly after that...

The mood was one of utter exhaustion and not just among the hacks: Juncker either batted away questions or handed them over to Rehn and Regling...The impression give was not of ten days to save the world but ten weeks or even months...No sense of dynamism or urgency.

The idea that there are just 10 days to save the euro was first floated in the Financial Times on Monday, and then repeated by Olli Rehn this morning. Of course, if the FT was right then we actually only have eight days left (unless it's a rolling deadline, ala George Osborne's fiscal mandate?....)

The word from Brussels is that the EU finance ministers' meeting is running around 90 minutes behind schedule....

...On his way into the meeting, Olli Rehn told reporters that he was optimistic that the International Monetary Fund might supply more money:

We are working towards having an increase of the IMF resources. We see very much eye-to-eye with the IMF's Christine Lagarde on this.

But will all IMF member states be as keen?.....

Now it's the turn of Herman Van Rompuy, president of the European Council, to sound the alarm. He just told a conference of EU ambassadors that Europe is trapped in a "systemic...full-blown confidence crisis."

Some may blame it on the irrationality of the market. But it's a fact and we need to confront it.

What's the solution? Van Rompuy argued that Europe must swallow closer fiscal union (as Germany, for example, has long demanded):

We need a significant step forward towards a real economic union commensurate with our monetary union.

Noon update: The full speech is now online here (pdf)

Interesting development in Italy this morning. The Italian Treasury has announced plans to "lend or borrow significant amounts of cash on the money markts", using its own account at the Bank of Italy.

The Italian Treasury describe it as "a new system of liquidity management" -- it seems that the Treasury will hold one-day auctions to either put more money into the Italian banking sector or take it out.

Izabella Kaminska of FT Alphaville compared it to the Supplementary Financing Program set up in America after the credit crunch. That was designed to soak liquidity out of the US banking sector (counterbalancing the huge injections from the Federal Reserve). The Italian scheme, though, would also seem designed to put liquidity into the system.

More as we get it....

11.05am UPDATE: The Italian Treasury announced it had assigned ?1.98bn in its first liquidity auction, at an average rate of 2%, having received bids of ?11.5bn from five banks. So today, at least, this new programme was used to get cash into the system....

...Izabella Kaminska has explained how it could also be used to loan government bills.

Just in case anyone was in doubt about the situation today, EU monetary effairs commissioner Olli Rehn has warned that Europe has just 10 days to "complete and conclude" its crisis response.

Commissioner Olli Rehn delivering his eurozone growth forecast in Brussels, in front of a backdrop spelling out his stark message. Photograph: Geert Vanden Wijngaert/AP

Commissioner Olli Rehn delivering his eurozone growth forecast in Brussels, in front of a backdrop spelling out his stark message. Photograph: Geert Vanden Wijngaert/AP Speaking ahead of today's EU finance ministers' meeting in Brussels, Rehn said Europe was now entering a "critical period":

We have to continue to work especially on two fronts -- both in order to ensure that we have sufficiently credible financial firewalls to contain market turbulence and at the same time we need to further reinforce our economic governance.

Meanwhile, ECB governing council member Christian Noyer also warned that the situation has deteriorated sharply in recent days. Noyer told a conference in Singapore that:

The situation in Europe and the world has significantly worsened over the past few weeks. Market stress has intensified .... (and) we are now looking at a true financial crisis -- that is a broad-based disruption in financial markets.

Incidentally (mainly for UK readers) my colleague Andrew Sparrow is tracking all the developments following yesterday's autumn statement in his Politics Live blog.

I'll be sticking to eurozone developments here. Please do flag up if we've missed anything interesting - I'm slightly playing catch-up after helping Andrew cover the autumn statement yesterday. It's very nice to be back.

The (limited) EFSF deal has not been well-received in the financial markets. The FTSE 100 fell 52 points (or just over 1%) in early trading to 5274, after Asian markets dropped across the board.

City traders say they are disappointed that eurozone finance ministers couldn't say how much firepower the EFSF now has. Wolfgang Sch?uble's admission that it won't reach ?1trn - and won't contain the crisis on its own - added to the let-down.

Michael Hewson, market analyst at CMC Markets, explained that:

We aren't really that much further forward given the lack of detail with respect to who is going to invest in the fund and how much the IMF will be involved.

As such the credibility gap remains.

German finance minister Wolfgang Sch?uble, pictured last month. Photograph: Ian Langsdon/EPA

German finance minister Wolfgang Sch?uble, pictured last month. Photograph: Ian Langsdon/EPA Wolfgang Sch?uble, Germany's finance minister, admitted last night that eurozone leaders had again failed to agree a way of expanding the EFSF up to the ?1tn target. That, he said, means the EFSF still cannot stem the debt crisis without IMF support.

From this morning's Daily Telegraph:

[Sch?uble] told Germany's Handelsblatt that although Europe needed a fund "capable of action", plans for the EFSF were too "intricate and complex" for investors to understand.

The finance ministers, who were meeting ahead of a full Ecofin summit today, acknowledged the ?440bn (?376bn) fund would not win support to leverage it up to ?1 trillion.

Its capacity would be betwen ?500bn and ?700bn instead ? a total that is unlikely to be big enough to rescue Spain and Italy.

You can read the official announcement of what was agreed last night in Brussels on the EFSF website.

It explains that the EFSF can now be used to guarantee between 20% and 30% of the full value of a bond issued by a eurozone member. That will allow the fund's assets to be 'leveraged' - as ?1bn of EFSF cash could underwrite more than ?3bn of new bonds.

The EFSF will also support the creation of "Co-Investment Funds (CIF)", made up of a mixture of public and private funding, and would again back the first tranche of potential losses.

But as we explained before (and as the Financial Times agrees here, IMF help is also going to be needed. The EFSF is already committed to helping Portugal and Ireland, as well as financing part of a second bailout for Greece.

With much of its ?440bn capacity already tied up in those commitments, there simply isn't a lot left to be leveraged.

Good morning, and welcome to another day of rolling coverage of the eurozone debt crisis.

Today's action is focused on Brussels, where late last night the 17 finance ministers from the eurozone agreed a deal to increase the firepower of the European Financial Stability Facility (EFSF).

But it appears that the plan does not give enough firepower to tackle the crisis.

Here's what my colleaugues David Gow and Ian Traynor filed overnight:

Klaus Regling, chief executive of the bailout find, the EFSF, admitted he could not "put a number" on its increased firepower as the ministers tacitly admitted it could not reach the promised ?1tn ? and instead returned to contested moves at the G20 summit in Cannes to increase the IMF's lending power. Officials had earlier said the EFSF would only reach some ?625bn compared with the current ?250bn left.

The clear aim is to get the IMF to come to the EFSF's rescue even though Regling insisted there was still plenty of appetite among outside investors for participating in the fund. Officials insist that sovereign wealth funds in Asia and hedge funds are among those still keen to invest while ministers approved a plan for the EFSF to guarantee the first 20-30% of loans to countries in trouble.

You can read the full story here.

Today, all 27 European Union finance ministers are gathering in Brussels. I'll be tracking developments from there with the help of colleages, and bringing expert analysis and reaction to the ongoing crisis. After a couple of days of optimism, we may be sinking back into the mire ...

Source: http://www.guardian.co.uk/business/blog/2011/nov/30/eurozone-crisis-finance-ministers-imf

case mccoy case mccoy kristin davis kristin davis phillies phillies philadelphia phillies

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.